Investment Strategies for Beginners: Building Your First Portfolio

Investing can seem intimidating for beginners, but it's one of the most powerful tools for building long-term wealth and achieving financial independence. With proper knowledge and strategy, anyone can start investing and benefit from the power of compound returns over time. This comprehensive guide will walk you through fundamental investment concepts, help you develop a personalized investment strategy, and provide practical steps to build your first investment portfolio with confidence.

Understanding Investment Fundamentals

Before diving into specific strategies, it's crucial to understand the basic principles that drive successful investing and wealth building over time.

The Power of Compound Returns

Compound returns represent the most powerful force in investing, where your investment gains generate their own gains over time. For example, $10,000 invested at 7% annual returns grows to approximately $76,000 over 30 years, with $56,000 of that growth coming from compounding rather than your original investment. Starting early maximizes the impact of compounding, making time your most valuable asset as an investor. Even small amounts invested consistently can grow into substantial wealth over decades.

Risk and Return Relationship

All investments involve some level of risk, and generally, higher potential returns come with higher risk. Understanding this relationship helps you make informed decisions about your investment choices. Conservative investments like government bonds offer lower returns but greater stability, while stocks offer higher potential returns with greater volatility. The key is finding the right balance for your risk tolerance, time horizon, and financial goals.

Inflation and Purchasing Power

Inflation erodes the purchasing power of money over time, making investing essential for maintaining and growing wealth. Historically, inflation averages around 3% annually, meaning money sitting in low-yield savings accounts actually loses purchasing power over time. Investments that can grow faster than inflation help preserve and increase your standard of living over the long term.

Setting Investment Goals and Timeline

Successful investing begins with clear goals and understanding your investment timeline, which determines your appropriate risk level and strategy.

Short-term vs. Long-term Goals

Short-term goals (less than 5 years) require more conservative investments to preserve capital, such as high-yield savings accounts, CDs, or short-term bond funds. Long-term goals (10+ years) can accommodate more aggressive investments like stocks, which may be volatile short-term but historically provide superior returns over extended periods. Medium-term goals (5-10 years) typically benefit from balanced approaches combining stocks and bonds.

Defining Your Risk Tolerance

Risk tolerance encompasses both your emotional ability to handle investment volatility and your financial capacity to absorb potential losses. Consider how you would react to seeing your portfolio drop 20-30% in value during a market downturn. If such losses would cause you to panic and sell, you may need a more conservative approach. Your risk tolerance should also reflect your financial situation – those with stable incomes and emergency funds can typically accept more risk than those with uncertain income or limited savings.

Creating SMART Investment Goals

Effective investment goals should be Specific, Measurable, Achievable, Relevant, and Time-bound. Instead of "save for retirement," a SMART goal might be "accumulate $500,000 in retirement accounts by age 60 through monthly contributions of $1,000." Clear goals help determine appropriate investment strategies and track progress over time. Consider multiple goals such as retirement, home purchase, children's education, or financial independence, each with its own timeline and strategy.

Types of Investment Accounts

Understanding different account types helps optimize your tax situation and maximize investment growth.

Taxable Investment Accounts

Taxable brokerage accounts offer maximum flexibility with no contribution limits or withdrawal restrictions, making them ideal for goals beyond retirement. You'll pay taxes on dividends and capital gains, but you can access your money anytime without penalties. These accounts work well for emergency funds beyond basic savings, medium-term goals, and additional investing after maximizing tax-advantaged accounts. Consider tax-efficient investments like index funds to minimize annual tax drag.

Tax-Advantaged Retirement Accounts

401(k) plans, traditional IRAs, and Roth IRAs offer significant tax advantages for retirement savings. Traditional accounts provide immediate tax deductions but require taxes on withdrawals, while Roth accounts use after-tax dollars but provide tax-free growth and withdrawals. Many employers offer 401(k) matching, providing immediate returns on your contributions. Maximize these accounts before investing in taxable accounts, as the tax advantages significantly boost long-term returns.

Specialized Accounts

Health Savings Accounts (HSAs) offer triple tax advantages for medical expenses and can serve as additional retirement accounts after age 65. 529 education savings plans provide tax-free growth for qualified education expenses. These specialized accounts can play important roles in comprehensive financial planning when used appropriately for their intended purposes.

Building a Diversified Portfolio

Diversification reduces risk by spreading investments across different asset classes, sectors, and geographic regions.

Asset Allocation Basics

Asset allocation involves dividing your portfolio among different asset classes like stocks, bonds, and cash. A common starting point for young investors is 80% stocks and 20% bonds, adjusting to more conservative allocations as you approach your goals. Within stocks, consider diversifying between domestic and international markets, large and small companies, and growth and value styles. Your specific allocation should reflect your risk tolerance, timeline, and goals.

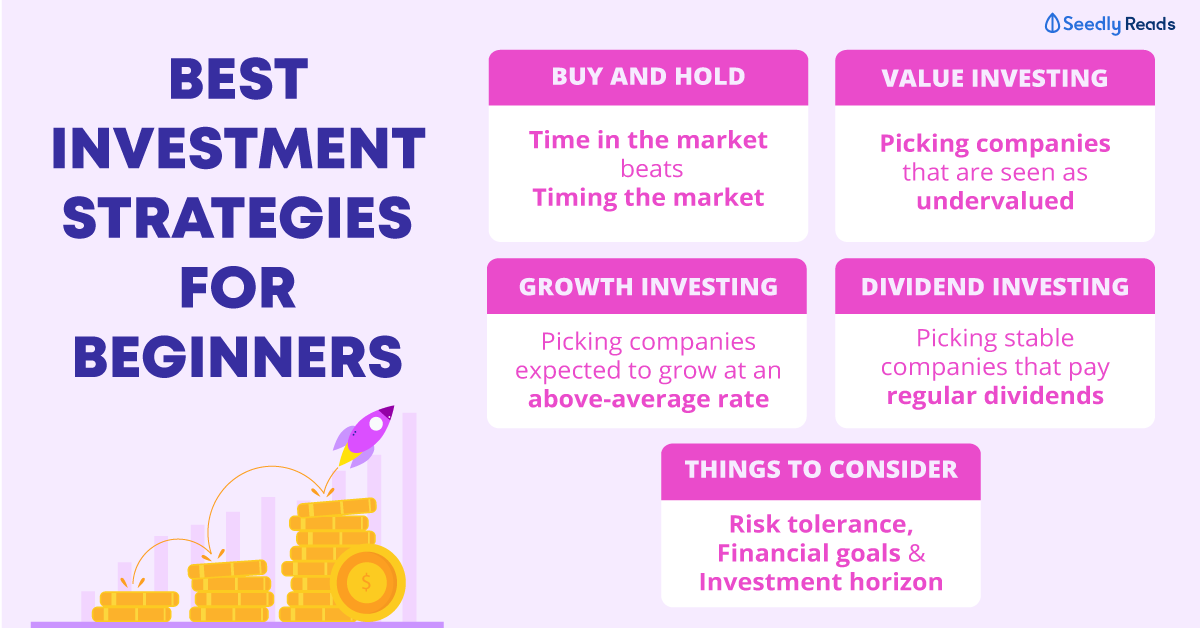

The Case for Index Funds

Index funds offer instant diversification at low costs, making them ideal for beginning investors. These funds track market indexes like the S&P 500, providing exposure to hundreds or thousands of companies with a single purchase. Index funds consistently outperform the majority of actively managed funds over long periods, primarily due to lower fees. A simple three-fund portfolio consisting of total stock market, international stock, and bond index funds can provide comprehensive global diversification.

Dollar-Cost Averaging Strategy

Dollar-cost averaging involves investing fixed amounts regularly regardless of market conditions, reducing the impact of market volatility over time. This strategy removes the pressure of timing the market and can result in lower average costs per share over time. Automate your investments through payroll deductions or automatic transfers to ensure consistency and remove emotional decision-making from the process.

Common Investment Options for Beginners

Understanding basic investment vehicles helps you make informed decisions about building your portfolio.

Individual Stocks

Stocks represent ownership shares in companies and offer the potential for high long-term returns. However, individual stock picking requires significant research and carries higher risk than diversified funds. If you choose to invest in individual stocks, limit them to a small portion of your portfolio and focus on companies you understand with strong competitive advantages. Consider blue-chip dividend-paying stocks for more conservative stock exposure.

Exchange-Traded Funds (ETFs)

ETFs combine the diversification of mutual funds with the trading flexibility of stocks. They typically have lower expense ratios than mutual funds and can be bought and sold throughout the trading day. ETFs cover virtually every asset class and investment strategy, from broad market indexes to specific sectors or themes. They're excellent tools for building diversified portfolios with relatively small amounts of money.

Bonds and Fixed Income

Bonds provide steady income and portfolio stability, serving as a counterbalance to stock volatility. Government bonds offer the highest safety but lowest returns, while corporate bonds provide higher yields with increased risk. Bond funds offer diversification across many individual bonds and professional management. Consider your overall portfolio allocation to bonds based on your risk tolerance and proximity to your investment goals.

Investment Platforms and Getting Started

Choosing the right investment platform and taking your first steps can seem overwhelming, but many excellent options exist for beginners.

Discount Brokerages

Major discount brokerages like Fidelity, Vanguard, and Charles Schwab offer commission-free stock and ETF trading with low account minimums. These platforms provide research tools, educational resources, and access to thousands of investment options. Compare expense ratios on funds, account fees, and available investment options when choosing a brokerage. Many offer target-date funds that automatically adjust allocation as you age, providing a simple hands-off approach.

Robo-Advisors

Robo-advisors like Betterment and Wealthfront provide automated portfolio management at low costs, making them excellent options for hands-off investors. These platforms use algorithms to create and rebalance diversified portfolios based on your goals and risk tolerance. While fees are higher than self-directed investing, they're much lower than traditional financial advisors and include automatic rebalancing and tax-loss harvesting.

Taking Your First Steps

Start by opening an account with a reputable brokerage or robo-advisor and making your first investment, even if it's a small amount. Many platforms have no minimum investment requirements, allowing you to start with as little as $1. Focus on building the habit of regular investing rather than trying to time the market or find the perfect investment. Consistency and time in the market are more important than timing the market perfectly.

Avoiding Common Beginner Mistakes

Understanding and avoiding common investment mistakes can save you significant money and stress over time.

Emotional Investing and Market Timing

Emotional decisions like panic selling during market downturns or buying during market peaks can severely damage long-term returns. Develop a written investment plan and stick to it regardless of market conditions. Remember that market volatility is normal and temporary, while long-term growth trends have historically been positive. Avoid checking your portfolio daily, as short-term fluctuations can trigger emotional responses that lead to poor decisions.

Lack of Diversification

Putting all your money in a single stock, sector, or asset class exposes you to unnecessary risk. Even successful companies can face unexpected challenges that devastate their stock prices. Diversify across asset classes, geographic regions, and company sizes to reduce risk while maintaining growth potential. Index funds and ETFs make diversification simple and affordable for investors with limited capital.

High Fees and Expenses

Investment fees compound over time just like returns, significantly impacting long-term wealth accumulation. A 1% annual fee might seem small, but it can reduce your portfolio value by 20% or more over 30 years compared to a 0.1% fee. Focus on low-cost index funds and ETFs, avoid frequent trading, and understand all fees associated with your investments and accounts. Even small fee differences can result in tens of thousands of dollars over long investment periods.

Conclusion

Successful investing doesn't require complex strategies or perfect market timing – it requires patience, consistency, and a long-term perspective. Start with simple, diversified investments like index funds, automate your contributions, and focus on time in the market rather than timing the market. The most important step is getting started, even with small amounts, and building the habit of regular investing.

Remember that investing is a marathon, not a sprint. Market volatility is normal and temporary, while the long-term trend of quality investments has historically been upward. Stay focused on your goals, continue learning, and resist the temptation to make emotional decisions based on short-term market movements. With proper strategy and patience, investing can help you build substantial wealth and achieve your financial goals over time.